BANGKOK, 9 November 2020: Dramatic changes are happening to new hotel development projects across Southeast Asia due to the severe Covid-19 triggered slowdown with global and regional chains rapidly shifting their attention to conversion opportunities and a management-light approach according to the latest C 9 Hotelworks research.

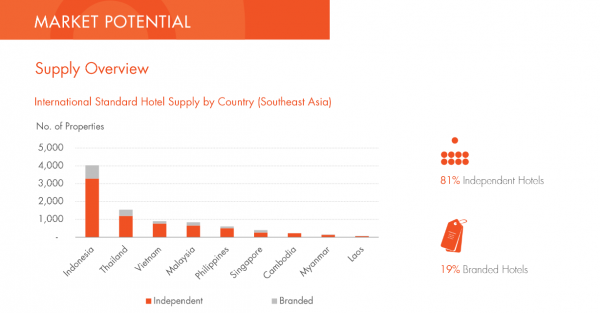

From a market size assessment, the stakes are high, according to data from STR, with over 80% of their reporting 8,757 international standard hotels in Southeast Asia classified as independent.

The recent Soft Brand Hotels Review research by hospitality consulting group C9 Hotelworks further notes that the top three countries in the region with the highest number of independent hotels are Vietnam, Indonesia and the Philippines.

Southeast Asia’s explosive hospitality growth trajectory over the past decade has been driven by developers new to the industry or those expecting hyper-tourism growth. This love affair with hotels has quickly soured in the wake of the pandemic, and suddenly owners are looking for stopgap measures for their multimillion-dollar assets as operating losses mount by the day.

“It’s ugly out there and about to get uglier,” says C9 Hotelworks Managing Director Bill Barnett. “Rising pressure from lenders and a mounting storm of unpredictability has set hotel owners adrift in a sea of economic uncertainty.

“This is especially prevalent in the midscale and upscale tiers, as most markets are domestic reliant, and seeing cheap deals at the top end of the market creates a domino effect across tiers. Bottom line, there simply is not enough broad demand to sustain Southeast Asia’s hotel sector, and the squeeze is felt directly where the largest room supply sits, in the middle.”

Another key hotel trend across the region highlighted in C9 Hotelworks’ research is the emergence of greater emphasis on soft brand offerings by global brands such as ACCOR, Marriott, and Hilton. This light approach takes in to account a growing number of owners who want their name reflected on properties and non-standardized design approaches. Add on the fast-track to conversions for operating properties or options to franchise for experienced developers, and there is clear evidence of major shifts in the industry.

Addressing the issue, C9’s Bill Barnett adds, “Southeast Asia’s hotel industry is being driven into a new cycle by the necessity generated by the pandemic, and common practices in North America and Europe that are now accelerating into the region. Our research shows fast development in franchising, third party operators, and a pivot by international chains to management-light approaches. Given the significant size of independent hotels, it’s a logical step to fish where the fish are.”

Summing up the post-Covid outlook, Delivering Asia Communications CEO David Johnson says “distribution and brand are on the cusp of a new disruptive cycle. While it’s a total departure from the standardized mass-market approach in recent times, it is without a doubt the shape of things to come.”

To download C9 Hotelworks report Soft Brand Hotels – Southeast Asia Market Review:

https://www.c9hotelworks.com/wp-content/uploads/2020/11/2020-11-soft-brand-hotel-market-review.pdf

You might also want to view C9 Hotelworks recent virtual online event on Soft Brands and White Label Hotels with leading hotel groups and experts speaking: https://www.youtube.com/watch?v=Ory2volCtJ8&t=1s