SINGAPORE, 5 July 2024: The International Air Transport Association (IATA) released May 2024 data for global passenger demand, highlighting positive passenger traffic for both international and domestic sectors.

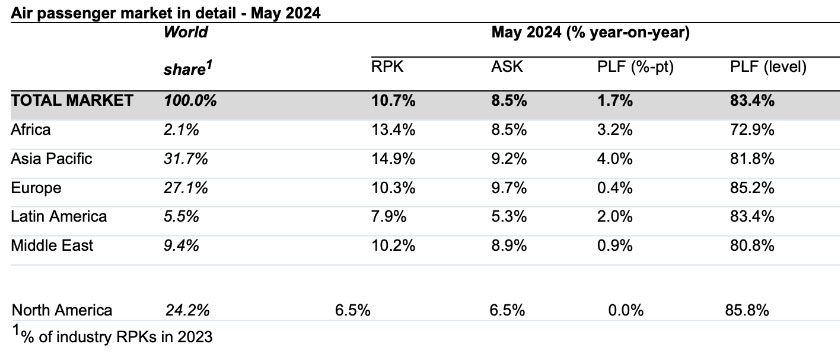

Total demand, measured in revenue passenger kilometres (RPKs), was up 10.7% compared to May 2023. Total capacity, measured in available seat kilometres (ASK), was up 8.5% year-on-year. The May load factor was 83.4% (+1.7ppt compared to May 2023), a record high for May.

International demand rose 14.6% compared to May 2023. Capacity was up 14.1% year-on-year, and the load factor improved to 82.8% (+0.3ppt on May 2023).

Domestic demand rose 4.7% compared to May 2023; capacity was up 0.1% year-on-year, and the load factor was 84.5% (+3.8ppt compared to May 2023).

“Strong demand for travel continues with airlines posting a 10.7% year-on-year increase in travel for May. Airlines filled 83.4% of their seats, a record for the month. With May ticket sales for early peak-season travel up nearly 6%, the growth trend shows no signs of abating. Airlines are doing everything they can to ensure smooth journeys for all travellers over the peak northern summer period,” said IATA’s Director General Willie Walsh.

“But our expectations of air navigation service providers (ANSPs) are already being tested. With 5.2 million minutes of air traffic control delays racked up in Europe even before the peak season begins, it is clear that Europe’s ANSPs have unresolved challenges. The 32,000 flight delays over the Memorial Day weekend in May show that challenges persist in the US, too. Airlines are accountable to their customers; ANSPs must be as well. ANSP performance matters to their airline customers and to millions of travellers. We all need them to do their job efficiently.”

Regional Breakdown – International Passenger Markets

All regions showed strong growth for international passenger markets in May 2024 compared to May 2023. The load factor increased in all regions except North America.

Asia-Pacific airlines continue to lead the way, with a 27.0% year-on-year increase in demand. Capacity increased 26.0% year-on-year and the load factor rose to 81.6% (+0.6ppt compared to May 2023). This performance maintains Asian carriers as the largest contributor to industry-wide growth in May, accounting for 42% of the year-on-year increase.

European carriers saw an 11.7% year-on-year increase in demand, an 11.3% year-on-year increase in capacity, and an 84.7% load factor (up 0.3ppt compared to May 2023).

Middle Eastern airlines saw a 9.7% year-on-year increase in demand. Capacity increased 9.0% year-on-year, and the load factor increased 0.5ppt to 80.7% compared to May 2023. Asian routes to the Middle East are particularly strong, now standing at 32% higher than in 2019. Another notable development is the Europe-Middle East route, which saw an April-May RPK increase for two years in a row, reversing the previous historical pattern of a decline between these months. In the coming months, it will become clearer to what extent these trends could be related to the Russia-Ukraine war.

North American carriers saw an 8.1% year-on-year increase in demand. Capacity increased 9.7% year-on-year, and the load factor fell to 84.0% (-1.2ppt compared to May 2023).

Latin American airlines saw a 15.9% year-on-year increase in demand, and capacity climbed 14.3% year-on-year. The load factor rose to 85.1% (+1.2ppt compared to May 2023), the region’s highest.

African airlines saw a 14.1% year-on-year increase in demand. Capacity was up 8.2% year-on-year. The load factor rose to 72.3% (+3.7ppt compared to May 2023). This was the fastest increase among all regions, although Africa still has the lowest load factor overall.

Domestic markets

Domestic demand increased at a stable pace in May. China’s growth rate surged in line with the post-Labour Day holidays. Japan declined 1.8%, possibly reflecting low business and consumer confidence.