SINGAPORE, 12 December 2024: Profitability will strengthen slightly for airlines during 2025 amid ongoing cost and supply chain challenges, the International Air Transport Association (IATA) reports in its latest financial outlook for the global airline industry.

2025 standouts

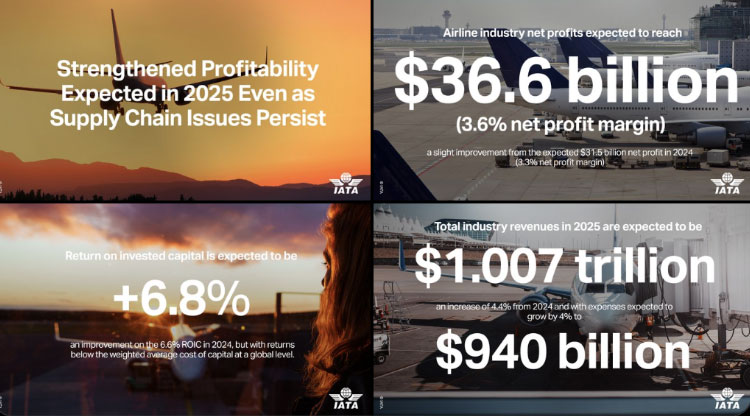

- Net profits should reach USD36.6 billion in 2025, representing a 3.6% net profit margin. That is a slight improvement from the expected USD31.5 billion net profit in 2024 (3.3% net profit margin). The average net profit per passenger is expected to be USD7.0 (below the USD7.9 high in 2023 but an improvement from USD6.4 in 2024).

- Operating profit in 2025 will total USD67.5 billion for a net operating margin of 6.7% (improved from 6.4% expected in 2024).

- The return on invested capital (ROIC) for the global industry is expected to be 6.8% in 2025. This is an improvement from the 2024 ROIC of 6.6%; the global industry returns remain below the weighted average cost of capital. ROIC is the strongest for airlines in Europe, the Middle East, and Latin America, where it did exceed the cost of capital.

- Total industry revenues should reach USD1.007 trillion. That is an increase of 4.4% from 2024 and will be the first time that industry revenues top the USD1 trillion mark. Expenses are expected to grow by 4.0% to USD940 billion.

- Passenger numbers are expected to reach 5.2 billion in 2025, a 6.7% rise compared to 2024 and the first time that the number of passengers has exceeded the five billion mark.

- Cargo volumes are expected to reach 72.5 million tonnes, a 5.8% increase from 2024.

“We’re expecting airlines to deliver a global profit of USD36.6 billion in 2025. This will be hard-earned as airlines take advantage of lower oil prices while keeping load factors above 83%, tightly controlling costs, investing in decarbonisation, and managing the return to more normal growth levels following the extraordinary pandemic recovery. All these efforts will help mitigate several drags on profitability outside of airlines’ control, namely persistent supply chain challenges, infrastructure deficiencies, onerous regulation, and a rising tax burden,” said IATA’s Director General Willie Walsh.

“In 2025, industry revenues will exceed USD1 trillion for the first time. It’s also important to put that into perspective. A trillion dollars is a lot—almost 1% of the global economy. That makes airlines a strategically important industry. But remember that airlines carry USD940 billion in costs, not to mention interest and taxes. They retain a net profit margin of just 3.6%. Put another way, the buffer between profit and loss, even in the good year that we are expecting in 2025, is just USD7 per passenger. With margins that thin, airlines must continue to watch every cost and insist on similar efficiency across the supply chain—especially from our monopoly infrastructure suppliers who all too often let us down on performance and efficiency,” said Walsh.

IATA highlighted the broad benefits of growing connectivity. The most recent estimates show that airline employment is expected to grow to 3.3 million in 2025. Airlines are the core of a global aviation value chain that employs 86.5 million people and generates USD4.1 trillion in economic impact, accounting for 3.9% of global GDP (2023 figures). Connectivity is an economic catalyst for growth in nearly all industries.

Outlook Drivers

Financial performance is expected to improve in 2025 due to lower jet fuel prices and efficiency gains. However, forced capacity discipline resulting from unresolved supply chain issues is holding back further increases. This limits growth opportunities and drives up several cost areas, including aircraft leasing and maintenance.

Net profitability will also be squeezed as airlines are expected to exhaust their tax loss carryovers from the pandemic era, leading to an increase in tax rates in 2025.

Revenue

Revenues are expected to grow by 4.4% to USD1.007 trillion in 2025. Passenger Revenues are expected to reach USD705 billion (70% of total revenue) in 2025, with an additional $145 billion (14.4% of total revenues) from ancillary services. Travel continues to become more affordable as the passenger yield is expected to fall by 3.4% (ticket and ancillaries). Unit revenues are expected to fall by a more moderate 2.5%.

Seen a different way, the average airfare in 2025, including ancillaries, is expected to be $380, 1.8% lower than in 2024. In real terms (adjusted for inflation), that represents a 44% drop compared to 2014, indicating that significant value is being passed to consumers in the industry’s continued effort to improve efficiency.

Passenger demand (RPKs) is expected to grow by 8.0% in 2025, which is ahead of a 7.1% expected expansion of capacity (ATK). Aircraft departures are forecast to reach 40 million, an increase of 4.6% from 2024, and the average passenger load factor is anticipated at 83.4%, up 0.4 percentage points from 2024.

Costs

Costs are expected to grow by 4.0% to USD940 billion in 2025.

Non-fuel: Higher costs were seen across the board in 2024, outside of fuel, putting pressure on margins. Key cost issues included intense salary pressure and one-off expenses related to several airline employee strikes in 2024. Additionally, aircraft groundings and an ageing global fleet have sharply increased maintenance costs. Overall non-fuel unit costs rose 1.3% in 2024 for a total of USD643 billion. Non-fuel unit cost increases in 2025 are expected to be limited to 0.5%, reaching USD692 billion.

The largest of the non-fuel costs is labour. In 2025, labour costs are expected to total $253 billion, up 7.6% from 2024. With productivity gains, however, average labour unit costs are likely to rise by only 0.5% in 2025 compared to 2024. The airline labour force is anticipated to rise by 4% to 3.3 million people.

Fuel: Jet fuel prices fell to USD70/barrel in September 2024 for the first time since the start of the Russia-Ukraine War. In 2025, jet fuel is expected to average USD87/barrel (down from USD99/barrel in 2024), based on a jet fuel crack spread of USD12 per barrel and a crude oil price of USD75/barrel (Brent). As a result, airlines’ cumulative fuel spend is expected to be USD248 billion, a decline of 4.8% despite a 6% rise in the amount of fuel expected to be consumed (107 billion gallons). Fuel is expected to account for 26.4% of operating costs in 2025, down from 28.9% in 2024.

The cost of compliance with CORSIA (purchasing carbon credits) started to be realised in 2024 and is estimated at USD700 million, rising to USD1 billion in 2025. The costs for the limited quantities of sustainable aviation fuel available are expected to add USD3.8 billion to industry fuel costs in 2025, up from USD1.7 billion in 2024.

Risks

With strong geopolitical and economic uncertainties, the most significant risks to the industry outlook include:

Conflict: A worsening of prospects should the wars in Europe and the Middle East spread. Conversely, achieving peace in either conflict is likely to have a positive impact, particularly in the case of the Russia-Ukraine War.

Trump Administration: The incoming Trump Administration in the US brings several significant uncertainties. Tariffs and trade wars would likely dampen air cargo demand and potentially impact business travel. Should these policies rekindle inflation with higher interest rates as a policy response, negative impacts on demand would be exacerbated. However, should the business-friendly stance of the first Trump administration continue into this term, gains from deregulation and business simplification could be significant. There is uncertainty regarding government support for aviation’s decarbonisation efforts in the US until the new administration’s path becomes clearer.

Oil Prices: Lower oil prices and fuel costs are a major driver of improved airline prospects in 2025. Should these not materialise for any reason, considering the industry’s thin margins, the outlook could change significantly.

Regional Roundup

All regions are expected to show improved financial performance in 2025 as compared to 2024, and all regions are expected to deliver a collective net profit in both 2024 and 2025. Profitability, however, varies widely by carrier and by region. For example, the collective net profit margin of African airlines is expected to be the weakest at 0.9% while carriers in the Middle East are most likely to be the strongest at 8.2%.

Asia Pacific is the largest market in terms of RPK, with China accounting for over 40% of the region’s traffic. In 2024, RPKs grew by 18.6%, fueled in part by market stimulus from visa requirement relaxations for entry to several countries, including China, Vietnam, Malaysia, and Thailand. Chinese carriers reported net losses in the first half of 2024 due to supply chain issues, over-supply in the domestic market, and a limitation of 100 weekly frequencies from China to the US (a third lower than pre-pandemic). Asia-Pacific has also experienced the sharpest drop in yields in 2024. Thanks to strong demand and increasing load factors, a slight improvement in profitability is likely in 2025.

For the full Global Outlook report: >Read the latest Global Outlook for Air Transport